All Categories

Featured

Table of Contents

[/image][=video]

[/video]

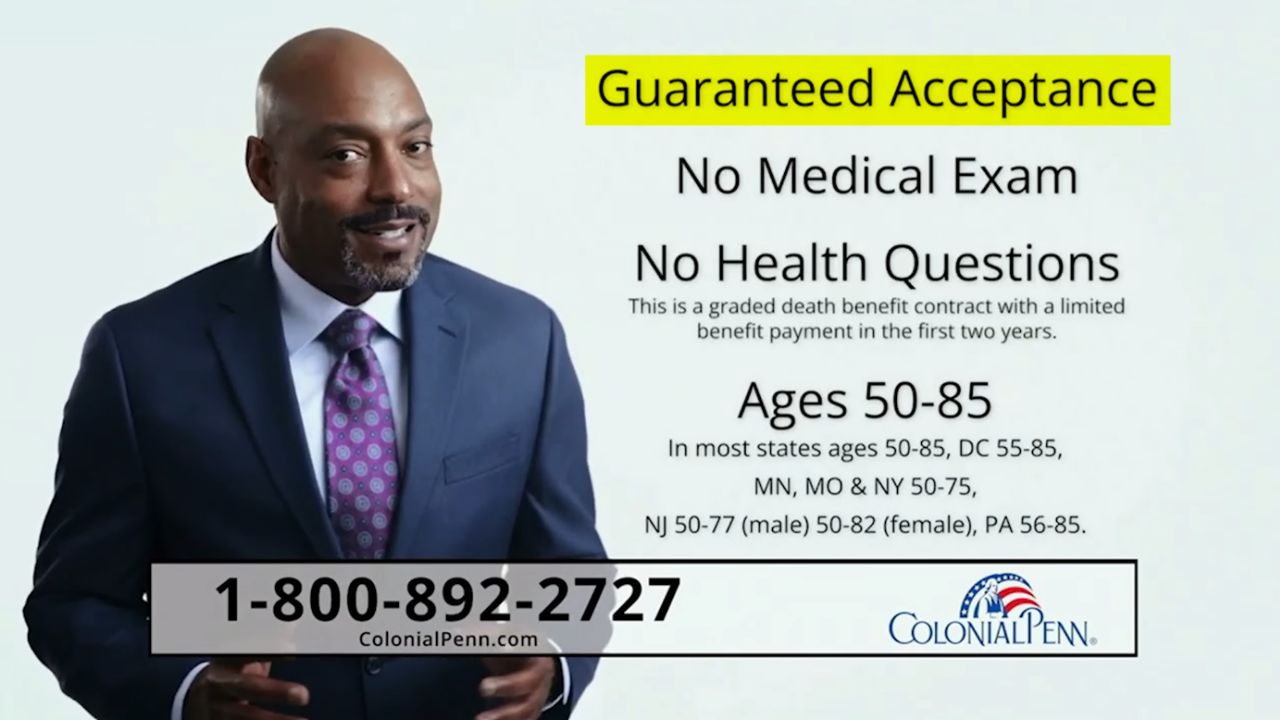

If you're in health and eager to undertake a medical examination, you might receive standard life insurance policy at a much lower expense. Guaranteed problem life insurance policy is frequently unnecessary for those healthy and can pass a medical examination. Because there's no medical underwriting, also those healthy pay the same premiums as those with health and wellness problems.

Offered the reduced protection quantities and higher premiums, guaranteed issue life insurance policy might not be the most effective choice for long-term financial preparation. It's typically more fit for covering last expenditures as opposed to replacing earnings or significant debts. Some guaranteed problem life insurance policies have age restrictions, often limiting candidates to a particular age variety, such as 50 to 80.

Nevertheless, assured problem life insurance policy includes higher premium costs compared to clinically underwritten plans, yet rates can vary substantially depending on variables like:: Various insurance policy business have various pricing models and may use various rates.: Older candidates will pay greater premiums.: Women frequently have reduced rates than men of the exact same age.

: The death benefit quantity impacts costs. A $25,000 policy expenses less than a $50,000 policy.: Paying premiums regular monthly costs much more general than quarterly or yearly payments.: Whole life premiums are higher general than term life insurance policy plans. While the assured problem does come at a price, it offers essential insurance coverage to those who might not get approved for generally underwritten policies.

Surefire concern life insurance coverage and simplified concern life insurance are both kinds of life insurance coverage that do not need a medical examination. Nevertheless, there are some crucial differences between the 2 kinds of plans. is a sort of life insurance that does not need any kind of wellness inquiries to be addressed.

Some Known Details About Term Life Insurance

Nonetheless, guaranteed-issue life insurance coverage policies usually have greater premiums and reduced fatality benefits than conventional life insurance policy policies. is a sort of life insurance that does call for some wellness inquiries to be addressed. The health inquiries are usually much less comprehensive than those asked for conventional life insurance policies. This means that streamlined concern life insurance coverage policies might be readily available to individuals with some wellness issues.

Today, underwriters can examine your details swiftly and involve a protection choice. In many cases, you could even have the ability to get immediate coverage. Instantaneous life insurance coverage is coverage you can obtain an immediate answer on. Your plan will begin as quickly as your application is accepted, suggesting the entire process can be carried out in less than half an hour.

Several web sites are promising instant insurance coverage that starts today, yet that doesn't mean every candidate will certify. Usually, customers will send an application believing it's for instantaneous coverage, just to be satisfied with a message they need to take a clinical exam.

The exact same info was after that utilized to authorize or deny your application. When you apply for an increased life insurance policy your information is examined instantaneously.

You'll then get instantaneous approval, split second being rejected, or notice you require to take a medical examination. There are several alternatives for instantaneous life insurance.

The 5-Minute Rule for Understanding Guaranteed Issue Life Insurance

The companies listed below offer totally online, straightforward choices. They all supply the opportunity of an instant decision. Ladder plans are backed by Fidelity Safety and security Life. The company supplies adaptable, immediate policies to people in between 18 and 60. Ladder policies allow you to make changes to your coverage over the life of your policy if your demands transform.

The firm uses plans to applications in between 21 and 55 for a ten-year term, and in between 21 and 45 for a 20-year term. Ethos policies are backed by Legal and General America.

Much like Ladder, you may need to take a medical examination when you request protection with Ethos. Nonetheless, the business says that the majority of applicants can get coverage without an examination. Unlike Ladder, your Principles policy will not start today if you require an exam. You'll need to wait up until your test results are back to obtain a price and purchase insurance coverage.

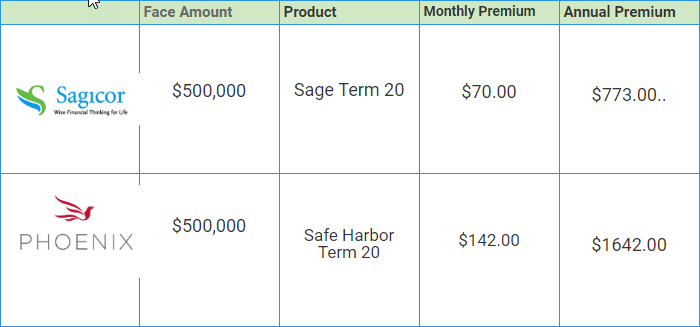

You may receive a choice promptly. In other cases, you'll need to supply even more info or take a clinical examination. Like Principles, you won't obtain a last cost or decision up until after the test is complete. Here is a rate contrast of insant life insurance for a half a century old male in excellent health.

The majority of individuals begin the life insurance policy buying policy by getting a quote. Allow's say you obtained a quote for $50 a month for a $500,000, 20-year policy.

Greater benefit amounts and longer terms will elevate your life insurance policy rates, while reduced benefit quantities and much shorter terms will reduce them. You can set the precise insurance coverage you're getting and after that start your application. A life insurance policy application will ask you for a whole lot of details. You'll require to give your health and wellness background and your household health background.

The Greatest Guide To Best No-medical-exam Life Insurance Companies

If the firm locates you didn't reveal information, your policy can be refuted. The decline can be mirrored in your insurance rating, making it tougher to get protection in the future.

A simplified underwriting policy will ask you detailed questions concerning your clinical background and current medical treatment during your application. An immediate concern plan will do the very same, but with the difference in underwriting you can get an immediate choice.

Second, the protection amounts are reduced, yet the premiums are usually higher. Plus, assured concern policies aren't able to be utilized throughout the waiting period. This indicates you can not access the complete survivor benefit quantity for a collection amount of time. For the majority of plans, the waiting duration is 2 years.

If you're in excellent health and wellness and can qualify, an instant problem plan will enable you to obtain coverage with no examination and no waiting duration. In that case, a streamlined issue policy with no exam may be best for you.

Not known Details About Guaranteed Issue Life Insurance

Remember that streamlined concern plans will certainly take a few days, while instant plans are, as the name implies, instant. Purchasing an instantaneous plan can be a fast and very easy procedure, yet there are a couple of things you should watch out for. Before you strike that purchase button make certain that: You're buying a term life policy and not an unintended fatality policy.

They don't offer coverage for disease. Some firms will provide you an unintentional death plan instantaneously yet require you to take a test for a term life plan.

Your agent has responded to all your concerns. Much like websites, some agents emphasize they can obtain you covered today without explaining or providing you the info you need.

{kind=link}

Table of Contents

Latest Posts

The smart Trick of No Medical Exam Life Insurance: Can I Get It? That Nobody is Talking About

The 9-Minute Rule for Find Out If Instant Life Insurance Is A Fit For You

The Ultimate Guide To No Exam Life Insurance Quote - Nationwide

More

Latest Posts

The smart Trick of No Medical Exam Life Insurance: Can I Get It? That Nobody is Talking About

The 9-Minute Rule for Find Out If Instant Life Insurance Is A Fit For You

The Ultimate Guide To No Exam Life Insurance Quote - Nationwide